Gallery

Table of contents

- Overview

- What are the primary mortgage options for non-residents in Dubai in 2026?

- Conventional Mortgages

- Islamic Mortgages (Sharia-Compliant Financing)

- Who is eligible for a non-resident mortgage in Dubai?

- Income and Employment Requirements

- Credit Score Impact

- Maximum Loan-to-Value (LTV) Ratios

- Understanding Key Mortgage Terms and Types

- Fixed vs. Variable Rates

- Mortgage Tenor and Age Restrictions

- The Dubai Mortgage Application Process for Non-Residents

- What documents are required for a non-resident mortgage application?

- Personal Identification and Visa Copies

- Bank Statements and Income Proof

- Property-Related Documents

- Are there specific challenges for non-resident borrowers?

- Currency Exchange Risks

Framework

- Overview

- What are the primary mortgage options for non-residents in Dubai in 2026?

- Conventional Mortgages

- Islamic Mortgages (Sharia-Compliant Financing)

- Who is eligible for a non-resident mortgage in Dubai?

Cluster links

Related in cluster

Comparative table

| Metric | Value | Note |

|---|---|---|

| Gross yield | Model range | Pre-cost metric |

| Net yield | Scenario range | After recurring costs |

| Liquidity | Medium to High | Exit depth |

| Legal safety | Scored | Title + process clarity |

| Tax efficiency | Profile-dependent | Investor jurisdiction |

Overview

Non-residents can indeed secure mortgages in Dubai for property purchases in 2026, though specific eligibility criteria, loan-to-value (LTV) ratios, and documentation requirements apply. Understanding these nuances is crucial for successfully navigating the market and securing favorable financing terms. What are the primary mortgage options for non-residents in Dubai in 2026? Who is eligible for a non-resident mortgage in Dubai? Understanding Key Mortgage Terms and Types The Dubai Mortgage Application Process for Non-Residents What documents are required for a non-resident mortgage application? Are there specific challenges for non-resident borrowers? Comparing Lenders: Banks Offering Non-Resident Mortgages What are the typical interest rates and fees in 2026? Tips for a Successful Non-Resident Mortgage Application

What are the primary mortgage options for non-residents in Dubai in 2026?

Non-residents typically have two primary mortgage options in Dubai: conventional mortgages and Sharia-compliant (Islamic) mortgages, each with distinct features and requirements. These options cater to a diverse range of financial preferences and ethical considerations for international investors.

Conventional Mortgages

Conventional mortgages in Dubai operate similarly to those in Western countries, involving interest-based lending where the bank provides funds for a property purchase, which the borrower repays with interest over a set period. They are widely available from both local and international banks operating in the UAE.

Islamic Mortgages (Sharia-Compliant Financing)

Islamic mortgages, known as Ijara or Murabaha, adhere to Sharia law, which prohibits interest (riba) and pure monetary speculation. Instead, the bank buys the property and then either leases it to the buyer with an option to purchase (Ijara) or sells it to the buyer at a higher, pre-agreed price (Murabaha), paid in installments.

Who is eligible for a non-resident mortgage in Dubai?

Eligibility for non-resident mortgages in Dubai in 2026 primarily depends on the borrower's income stability, credit history, age, and the property's value. Banks assess these factors rigorously to mitigate risk associated with overseas lending.

Income and Employment Requirements

Non-resident applicants must demonstrate a stable and verifiable income, typically requiring a minimum monthly salary (or equivalent) in a reputable currency, and proof of employment stability. Banks generally prefer applicants who have been employed for at least two years and can provide detailed bank statements.

Credit Score Impact

While international credit scores can be considered, Dubai banks primarily evaluate an applicant's financial health through their income, existing liabilities, and potentially through credit reports from their home country or international agencies. A strong financial standing without excessive debt is crucial.

Maximum Loan-to-Value (LTV) Ratios

The maximum Loan-to-Value (LTV) for non-resident mortgages in Dubai is generally lower than for residents, often capped at 50% for properties valued above AED 5 million and 60% for properties valued below AED 5 million. This means a larger down payment is required from the borrower.

Understanding Key Mortgage Terms and Types

Familiarity with critical mortgage terms such as interest rates, tenor, and repayment structures is essential for non-residents to make informed decisions about their Dubai property financing.

Fixed vs. Variable Rates

Non-resident mortgages can come with either fixed interest rates, which remain constant for an initial period (e.g., 1-5 years), or variable rates, which fluctuate with market benchmarks like EIBOR (Emirates Interbank Offered Rate). Fixed rates offer stability, while variable rates may offer lower initial payments but carry market risk.

Mortgage Tenor and Age Restrictions

The maximum mortgage tenor for non-residents in Dubai typically ranges from 15 to 25 years, and borrowers must usually repay the mortgage by the age of 65 to 70. This impacts monthly repayments and the total interest paid over the loan term.

The Dubai Mortgage Application Process for Non-Residents

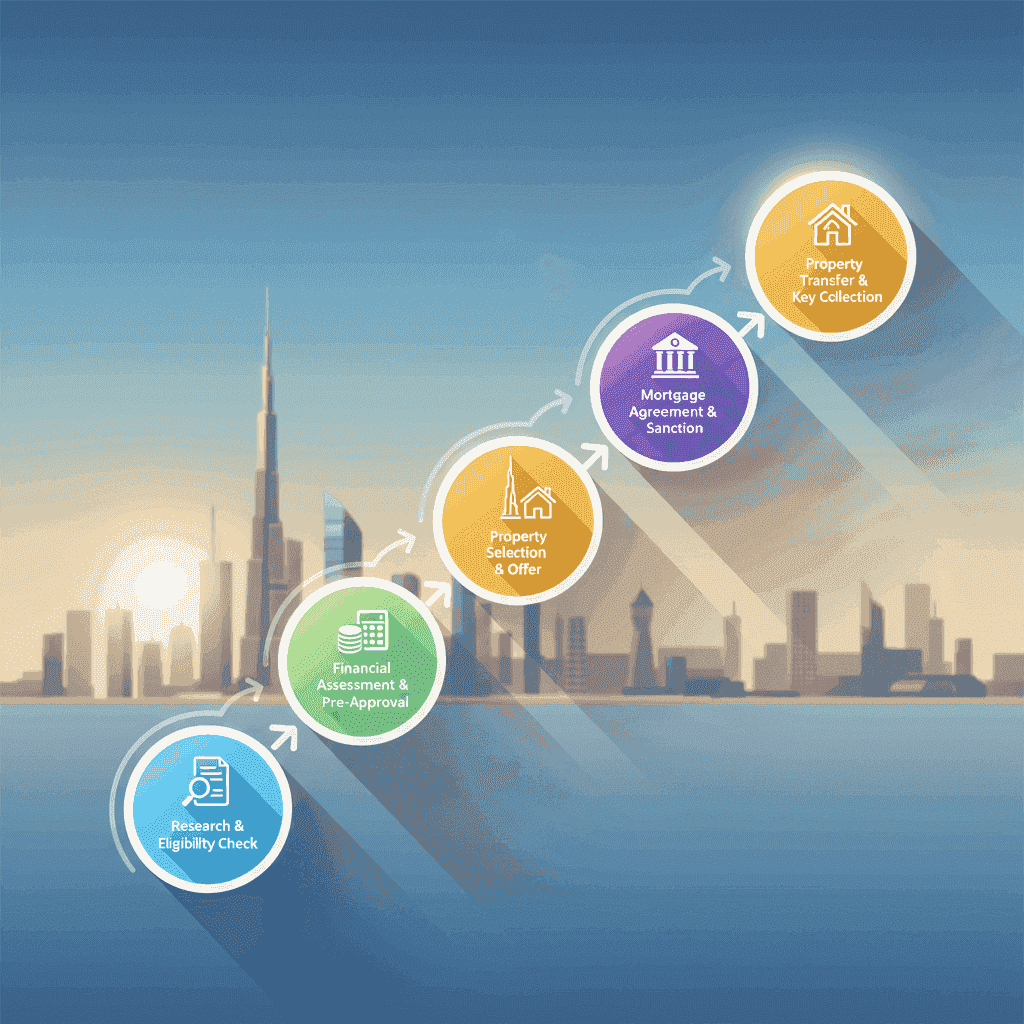

The application process for a non-resident mortgage in Dubai involves several key steps, from initial pre-approval to final registration, requiring meticulous documentation and clear communication with lenders. Initial Consultation and Pre-Approval: Begin by consulting with a mortgage broker or bank to understand eligibility and obtain a pre-approval, which gives an indication of the maximum loan amount you can borrow. This step involves an initial assessment of your financial standing and required documentation. Property Selection and Offer: Once pre-approved, identify a suitable property in Dubai and make an offer, securing a Memorandum of Understanding (MOU) or Sales Purchase Agreement (SPA) with the seller. This legal document outlines the terms of the sale. Full Application Submission: Submit your complete set of required documents to the chosen bank for a full mortgage application. Ensure all financial statements, proof of income, and personal identification are up-to-date and accurately presented. Property Valuation and Approval: The bank will arrange for an independent valuation of the chosen property to confirm its market value, followed by their final approval of your mortgage application. The valuation fee is typically borne by the buyer. Loan Offer and Signing: Upon approval, the bank will issue a formal loan offer, outlining all terms, conditions, interest rates, and repayment schedules. Carefully review and sign this agreement. Property Registration and Disbursement: The final step involves registering the property with the Dubai Land Department (DLD) and the bank disbursing the loan amount to the seller, completing the transaction. Ensure all DLD fees are accounted for.

What documents are required for a non-resident mortgage application?

Non-residents must provide a comprehensive set of documents, including personal identification, proof of income and assets, and property-related paperwork, to support their mortgage application in Dubai.

Personal Identification and Visa Copies

You will need copies of your passport, visa (if applicable for entry into UAE), and proof of residential address in your home country. Some banks may also request a UAE entry stamp.

Bank Statements and Income Proof

Provide recent bank statements (typically 6-12 months) from your primary bank account, along with employment contracts, salary certificates, and audited financial statements if self-employed. This validates your income stream.

Property-Related Documents

Required property documents include the Memorandum of Understanding (MOU) or Sales Purchase Agreement (SPA), Title Deed copy, and Oqood (for off-plan properties) where applicable.

Are there specific challenges for non-resident borrowers?

Non-resident borrowers in Dubai may face challenges such as lower LTV ratios, stringent documentation requirements, potential currency exchange risks, and a need for local legal understanding.

Currency Exchange Risks

Since income is typically earned in a foreign currency, fluctuations in exchange rates against the AED can impact the real cost of mortgage repayments. Hedging strategies or stable income sources can mitigate this risk.

Actionable conclusion

Staying informed about Dubai's real estate market trends, economic forecasts, and regulatory changes for 2026 will help in making strategic property and financing decisions. For broader insights, consider resources like those on Bali Property Investment Opportunities for comparison.